Energy - Oil - Economy

It's incredible how short-sighted people are today. Oil prices decline for a few weeks and OPEC starts talking about a production cut, Chevron puts tar sand projects expansion on hold; and people start driving their SUVs again.

Folks, it's TEMPORARY. First, the oil tycoons want to keep Republicans in office. They give 11 times as much in campaign contributions to Republicans as they do their opponents because they like the status quo. They also know an election is coming up in just a few days and that high gasoline prices will encourage people to vote Republicans out of office, particularly if they've lost a job or a son in Iraq.

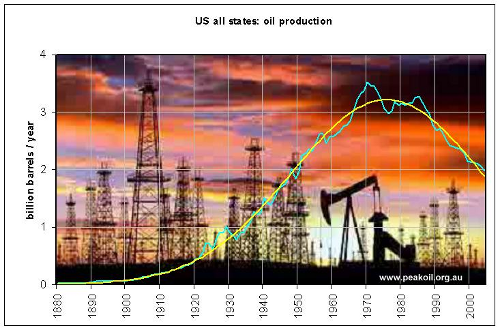

About this Hubbert curve crap; the theory being that the peak happens when half the oil is pumped out; that's just crap. There is a lot of oil in the ground, much more than has been pumped out. The problem is that the light sweet crude (requiring minimal refining) close to the surface under pressure (so you don't have to expend energy to pump or otherwise force it out) in giant pools (so one can get a lot of return on discovery investments) is gone.

What remains near the surface is heavy sour crude. Heavy crude is crude with a heavy mix of long chain hydrocarbons which has a very high viscosity sometimes requiring heat or solvents to get it to flow. Sour crude is crude with a high sulfur content requiring additional sulfur removal steps in the refinery process. Heavy crude also requires cracking and reforming to convert long-chain hydrocarbons to shorter more commercially valuable hydrocarbons. This takes additional energy and in extreme cases you can end up using the energy equivalent of five barrels of oil to produce one barrel of refined product.

Manufacturing the necessary drilling rigs to drill deep takes time, upgrading our refineries takes time. Even with the necessary upgrades it still costs more to produce and refine this oil than it did the light sweet crude near the surface that existed in the past. We really must start thinking of energy in terms of sources other than fossil fuels.

Our flavor of capitalism which utilizes money created by a private banking consortium which is loaned to our economy at interest, requires constant economic expansion to pay that interest. Constant economic expansion requires a constant expansion of energy supply, which, if we continue to rely on oil, can't continue indefinitely at the required rate. The growing economies of India and China exacerbate this problem by placing additional demand on limited oil supplies.

Until we adequately address our energy needs, we are going to see extreme instability in the economy where the economy grows until it runs into an energy wall, energy prices rise precipitously, our economy shrinks rapidly, the demand decreases, and then prices fall, and the cycle repeats itself. But as India and China continue to grow economically, and as inexpensive oil supplies continue to shrink, with each cycle we'll see less economic growth, higher energy prices, and a deeper depression following the rise in prices.

The best time to put alternatives in place is now; as time goes on we will have less and less energy and capital available to make the necessary infrastructure changes.

Now is the time to modernize our electrical grid converting all long distance lines longer than 300km from AC to DC transmission. This step alone save the energy equivalent of all the oil we import. At night we can not throttle down electricity production as much as demand decreases. If we used all of this surplus electricity to recharge plug-in hybrids and used that for our daily commute; we could eliminate again the energy equivalent of all the oil we import. Between these two things we could eliminate more than the energy equivalent of all of the oil we consume.

There is more that we can do, wind power is less expensive than even coal fired power stations. The argument is that we can't use more than about 20% wind power on the grid and that we must back any added wind capacity with an equivalent amount of base power generation. This is simply untrue; if we have a modernized grid capable of sending energy anywhere in the country, geographical diversity will allow us to depend upon about 30% of the installed wind capacity. That is, the wind is always blowing somewhere, and the minimum amount generated is about 30% of the capacity if you have reasonable geographical diversity.

There are ways we can use the excess to better effect when we are making more electricity than we need, we can make aluminum, we can electrolyze water into hydrogen and oxygen, we can store energy in large Redox battery systems which use oxides of vanadium as liquid electrodes, we can pump water up hill and run it through turbines to drive generators later.

If we were to go to a real-time metering systems in which the cost of energy varied with supply and demand, people and industries would shift their consumption habits to better match availability. People would do things like shift their laundry to times when energy costs are lower, install larger water tanks and heat water during off-peak periods, construct homes with larger thermal mass and other passive devices that will allow them to utilize less energy and time their usage to lower usage periods.

Instead of building a super highway between Mexico and Canada up the middle of the United States, we should be expanding and electrifying our railroads. We need to have a way to continue moving food and goods across our country when the oil runs out. If we wait too long to put this infrastructure in place; a lot of people are going to starve to death.

There are people who say that it's not possible to replace fossil fuels with renewables, that they aren't scalable enough. That is just hogwash. I've looked at this problem and we have ample renewable resources requiring no new technological breakthroughs. We could power this country off of geo-thermal, solar, or wind alone many times over, however, none of these can be ramped up instantly, neither can our automobile, train, and aircraft fleet be replaced instantly, so we really must do everything we can.

We should start developing our geo-thermal resources rapidly, particularly I think we could kill two birds with one stone and over time decrease volcanic hazards in some areas like Near Mt. Rainier or Yellowstone. Geo-thermal has the advantage of being "baseload" power, that is it is available 24x7 and not just when the wind blows or the sun shines.

We should build actinide burning fast-flux reactors and place them inside the hollowed out Yucca mountain repository; along with intergral pyrolytic reprocessing facilities so that we can get rid fo the long term radioactive waste instead of merely storing it, and derive huge amounts of energy in the process, approximately 100 times as much as was released in the initial one pass through a boiling water reactor.

Low grade heat from the fission products that remain could be used for everything from industrial source heat to home heating. Since the Yucca Mountain repository was designed for the long-term storage of waste; in the event of an accident in one of these reactors, the radioactive contamination would be contained as well.

We can have the largest depression this country has ever seen, with no recovery and the bulk of our population starving, or we can have a robust economy, a clean environment, and a comfortable sustainable future. It is our choice, but we are rapidly approaching the point where we will no longer have the necessary resources to build new infrastructure and then the choice will be taken from us. We can not allow our oil company owned politicians to steal our future from us.

Folks, it's TEMPORARY. First, the oil tycoons want to keep Republicans in office. They give 11 times as much in campaign contributions to Republicans as they do their opponents because they like the status quo. They also know an election is coming up in just a few days and that high gasoline prices will encourage people to vote Republicans out of office, particularly if they've lost a job or a son in Iraq.

About this Hubbert curve crap; the theory being that the peak happens when half the oil is pumped out; that's just crap. There is a lot of oil in the ground, much more than has been pumped out. The problem is that the light sweet crude (requiring minimal refining) close to the surface under pressure (so you don't have to expend energy to pump or otherwise force it out) in giant pools (so one can get a lot of return on discovery investments) is gone.

What remains near the surface is heavy sour crude. Heavy crude is crude with a heavy mix of long chain hydrocarbons which has a very high viscosity sometimes requiring heat or solvents to get it to flow. Sour crude is crude with a high sulfur content requiring additional sulfur removal steps in the refinery process. Heavy crude also requires cracking and reforming to convert long-chain hydrocarbons to shorter more commercially valuable hydrocarbons. This takes additional energy and in extreme cases you can end up using the energy equivalent of five barrels of oil to produce one barrel of refined product.

Manufacturing the necessary drilling rigs to drill deep takes time, upgrading our refineries takes time. Even with the necessary upgrades it still costs more to produce and refine this oil than it did the light sweet crude near the surface that existed in the past. We really must start thinking of energy in terms of sources other than fossil fuels.

Our flavor of capitalism which utilizes money created by a private banking consortium which is loaned to our economy at interest, requires constant economic expansion to pay that interest. Constant economic expansion requires a constant expansion of energy supply, which, if we continue to rely on oil, can't continue indefinitely at the required rate. The growing economies of India and China exacerbate this problem by placing additional demand on limited oil supplies.

Until we adequately address our energy needs, we are going to see extreme instability in the economy where the economy grows until it runs into an energy wall, energy prices rise precipitously, our economy shrinks rapidly, the demand decreases, and then prices fall, and the cycle repeats itself. But as India and China continue to grow economically, and as inexpensive oil supplies continue to shrink, with each cycle we'll see less economic growth, higher energy prices, and a deeper depression following the rise in prices.

The best time to put alternatives in place is now; as time goes on we will have less and less energy and capital available to make the necessary infrastructure changes.

Now is the time to modernize our electrical grid converting all long distance lines longer than 300km from AC to DC transmission. This step alone save the energy equivalent of all the oil we import. At night we can not throttle down electricity production as much as demand decreases. If we used all of this surplus electricity to recharge plug-in hybrids and used that for our daily commute; we could eliminate again the energy equivalent of all the oil we import. Between these two things we could eliminate more than the energy equivalent of all of the oil we consume.

There is more that we can do, wind power is less expensive than even coal fired power stations. The argument is that we can't use more than about 20% wind power on the grid and that we must back any added wind capacity with an equivalent amount of base power generation. This is simply untrue; if we have a modernized grid capable of sending energy anywhere in the country, geographical diversity will allow us to depend upon about 30% of the installed wind capacity. That is, the wind is always blowing somewhere, and the minimum amount generated is about 30% of the capacity if you have reasonable geographical diversity.

There are ways we can use the excess to better effect when we are making more electricity than we need, we can make aluminum, we can electrolyze water into hydrogen and oxygen, we can store energy in large Redox battery systems which use oxides of vanadium as liquid electrodes, we can pump water up hill and run it through turbines to drive generators later.

If we were to go to a real-time metering systems in which the cost of energy varied with supply and demand, people and industries would shift their consumption habits to better match availability. People would do things like shift their laundry to times when energy costs are lower, install larger water tanks and heat water during off-peak periods, construct homes with larger thermal mass and other passive devices that will allow them to utilize less energy and time their usage to lower usage periods.

Instead of building a super highway between Mexico and Canada up the middle of the United States, we should be expanding and electrifying our railroads. We need to have a way to continue moving food and goods across our country when the oil runs out. If we wait too long to put this infrastructure in place; a lot of people are going to starve to death.

There are people who say that it's not possible to replace fossil fuels with renewables, that they aren't scalable enough. That is just hogwash. I've looked at this problem and we have ample renewable resources requiring no new technological breakthroughs. We could power this country off of geo-thermal, solar, or wind alone many times over, however, none of these can be ramped up instantly, neither can our automobile, train, and aircraft fleet be replaced instantly, so we really must do everything we can.

We should start developing our geo-thermal resources rapidly, particularly I think we could kill two birds with one stone and over time decrease volcanic hazards in some areas like Near Mt. Rainier or Yellowstone. Geo-thermal has the advantage of being "baseload" power, that is it is available 24x7 and not just when the wind blows or the sun shines.

We should build actinide burning fast-flux reactors and place them inside the hollowed out Yucca mountain repository; along with intergral pyrolytic reprocessing facilities so that we can get rid fo the long term radioactive waste instead of merely storing it, and derive huge amounts of energy in the process, approximately 100 times as much as was released in the initial one pass through a boiling water reactor.

Low grade heat from the fission products that remain could be used for everything from industrial source heat to home heating. Since the Yucca Mountain repository was designed for the long-term storage of waste; in the event of an accident in one of these reactors, the radioactive contamination would be contained as well.

We can have the largest depression this country has ever seen, with no recovery and the bulk of our population starving, or we can have a robust economy, a clean environment, and a comfortable sustainable future. It is our choice, but we are rapidly approaching the point where we will no longer have the necessary resources to build new infrastructure and then the choice will be taken from us. We can not allow our oil company owned politicians to steal our future from us.

From a fundamental supply/demand standpoint, the outlook for higher crude oil prices in 2011 was already expected, with prices having moved up 12% in the fourth quarter of 2010 largely because of the strengthening U.S. and global economies.3 However, the majority of the increase in crude oil prices in recent weeks has been due to an increased “risk premium” for the commodity, which reflects the possibility of political unrest spreading to additional and particularly larger crude oil producers in the region.

From a fundamental supply/demand standpoint, the outlook for higher crude oil prices in 2011 was already expected, with prices having moved up 12% in the fourth quarter of 2010 largely because of the strengthening U.S. and global economies.3 However, the majority of the increase in crude oil prices in recent weeks has been due to an increased “risk premium” for the commodity, which reflects the possibility of political unrest spreading to additional and particularly larger crude oil producers in the region.

price hype, oil revenues stood at U$19.7bn, according to

price hype, oil revenues stood at U$19.7bn, according to